We take a look into the Kelly criterion, created by John L. Kelly, which is a mathematical formula used by both gamblers and investors to determine the best position size.

Figuring out the best position size for a trade can be challenging. Careful investors usually bet small, which significantly reduces their profit potential. On the other hand, while betting big could let you take home big winnings, it can also cost you dearly. The below meme is common in investing communities, where traders bet too much on a single trade, and end up losing a lot of money or getting liquidated.

The Kelly criterion was developed to determine how much to invest in a certain asset, how much to bet on horse racing, or the optimal bet size at the blackjack table.

Join us in showcasing the cryptocurrency revolution, one newsletter at a time. Subscribe now to get daily news and market updates right to your inbox, along with our millions of other subscribers (that’s right, millions love us!) — what are you waiting for?

What Is the Kelly Criterion?

The Kelly criterion is a mathematical formula to maximize wealth growth over time. Originally developed to study the disturbances in long-distance phone calls, the formula was quickly adopted by professional gamblers to calculate the optimal betting size.

Since then, sophisticated traders and investors alike use the formula to plan and manage their portfolio, in order to maximize the profit potential – a strategy that has proven successful over time.

History of the Kelly Criterion

The popular gambling and investing formula was developed by John L. Kelly while working at telecommunications company AT&T.

Kelly’s role at the company was to analyze disturbances in long-distance calls. After he first published his findings in the 1956 academic paper “A new interpretation of information rate,” it did not take long for professional gamblers to adopt the formula in a different, albeit less academic, setting: determining how much to bet on horse races.

Today, it is widely used as a general money and portfolio management system in sports betting, gambling, trading and investing.

How Is the Kelly Criterion Calculated?

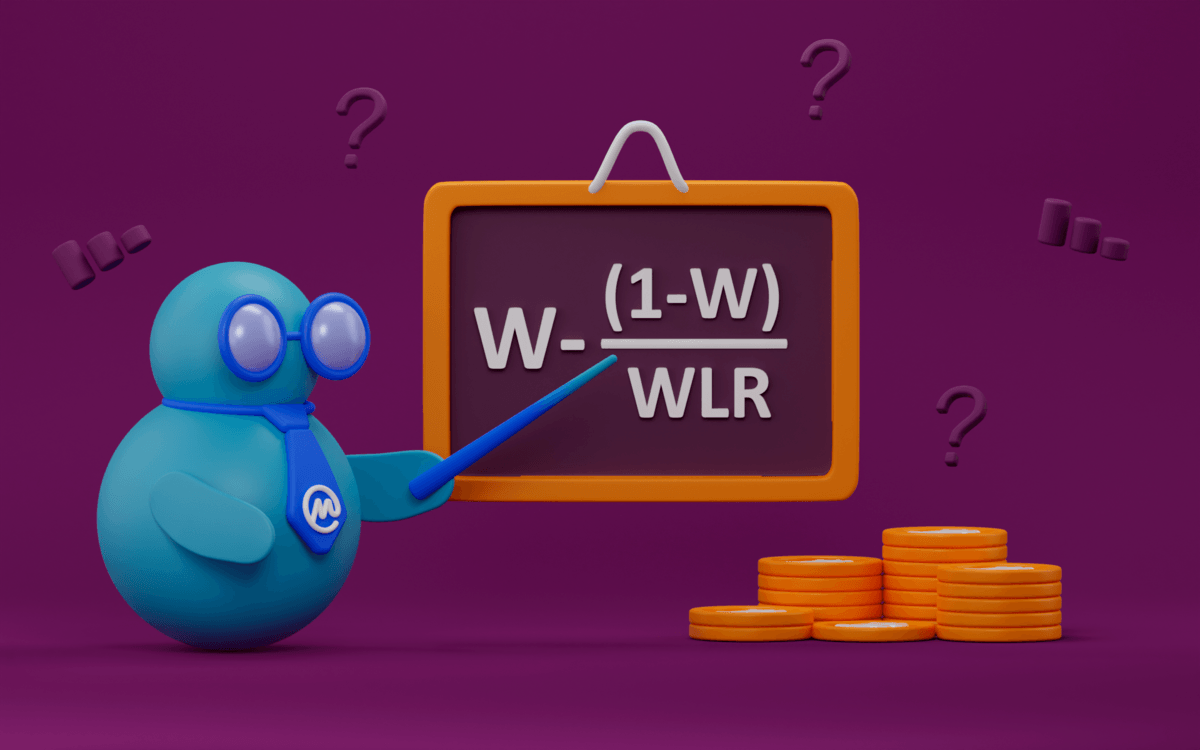

The Kelly formula consists of two basic components. It considers the likelihood of the gamble or investment resulting in a win (W), as well as the win/loss ratio (WLR): the average gain of a winning trade, divided by the average loss on a losing trade.

These inputs are then fed into the Kelly equation:

The output of the mathematical formula is known as the Kelly percentage, which investors and gamblers use to determine how much of their bankroll or portfolio to allocate to a bet – maximizing their expected return.

How Do You Input Odds Into the Kelly Criterion?

Determine your win rate, and your win-loss ratio, using the following calculations:

Win rate: Divide the number of wins, by the total number of trades taken.

Win-Loss Ratio: Divide your average gain by your average loss.

Once you have those data points, you can calculate the Kelly Percentage by feeding the outcomes into the formula.

How To Use the Kelly Criterion in Trading

To put the Kelly system to work, you will need data on your performance. Seasoned traders use a trading journal, and if you do not track your trades yet, the best time to start is now. Alternatively, you could backtest your strategy.

Once you have data on your last 50 to 60 trades, we can get to work. The first step is to calculate your win rate (W). This is done by dividing the number of wins, by the total number of trades taken. From there, the next step is to calculate the WLR, by dividing your average gain by your average loss.

Once you have those data points, you can calculate the Kelly Percentage by feeding the outcomes into the formula we discussed earlier.

Interpreting the Results

After making the necessary calculations, the Kelly formula will provide you with a percentage to risk on each trade, gamble, or investment. For example, if the outcome of the formula is 0.035, you should risk 3.5% of your bankroll on each bet.

In some cases, you may have to overrule the Kelly strategy. Regardless of the outcome of the calculation, it is unwise to risk more than 20% on a single position, bet or trade. Going over this limit carries more risks than any smart investor would willingly take.

Is the Kelly Criterion Effective?

The Kelly strategy is a mathematical approach to money management and maximizing your returns. Because the approach is founded in telecommunications theory, many people question its real-world applicability to the stock market or gambling.

However, doubters can simply input their current data and project the trajectory of their account if they would use the Kelly criterion. So long as they follow the same trading system, and the data is entered into the formula correctly, the real-world performance should not be much different from the projections.

How Do I Find My Win Probability With the Kelly Criterion?

While most casino games and other forms of gambling have very clear and structured odds, there is no fool proof way of calculating the odds of a given trade or investment. Therefore, most traders and investors rely on their historical performance to calculate the win rate.

Though not 100% accurate, if a trader is able to maintain a consistent average win rate over extended periods of time, it is reasonably safe to assume this will continue.

What Is Better Than the Kelly Criterion?

Even though many investors have managed to build a successful portfolio on the principles of the Kelly criterion, it is not a guarantee to success.

The Kelly criterion is aimed at seeking optimal returns, but some investors are more focused on minimizing risk, while others are saving for a specific goal, such as their retirement. Therefore, the Kelly formula may not be suited for certain investors, while it is very successful for others.

How Are the Black-Scholes Model, the Kelly Criterion, and the Kalman Filter Related?

The Kalman filter, the Kelly criterion and the Black-Scholes model all play a different role in portfolio management. Using more than one of them is therefore not unheard of.

Namely, the Black-Scholes model is used to calculate the theoretical value of an option contract, based on how much time is left until maturity, and a few other factors. Meanwhile, the Kalman filter estimates the value of unknown variables, where more precise measurements are impossible.

Essentially, they are three different popular mathematical formulas used to calculate the returns of an investment.

What Is a Good Kelly Ratio?

As discussed earlier, it is unwise to follow the Kelly percentage if it is higher than 20%, because this puts the trader at unnecessary investment risk. Therefore, some investors like to use less than the Kelly percentage (for instance, half of what their Kelly ratio is). This risk-averse approach is often referred to as a fractional Kelly bet.

In some cases, the Kelly formula produces a percentage of lower than zero, which means the formula does not recommend betting at all. In these cases, it is best to reconsider the strategy, as it does not produce many results.

The Kelly Criterion Formula in Gambling

Using the Kelly criterion formula in gambling is straightforward, as the odds are reasonably clear from the start and relatively simple to understand. For example, the odds of hitting red in roulette are approximately 48% and the odds of guessing the number right 2.7%.

This makes it easy to apply the Kelly formula in gambling – the odds are already known. Simply insert the data into the formula and get to work.

The Kelly Criterion Formula in Investing

Contrary to gambling and casino games, trades and investments do not have a similarly clear odds structure. In fact, the odds are hard to tell in advance at all – which is why most traders rely on historical performance to calculate their win rate.

This makes applying the Kelly formula in trading and investing slightly more complicated, but with a few simple calculations, the formula can be applied here as well.

Does Warren Buffett Use the Kelly Criterion?

Warren Buffett deserves at least partial credit for the popularity of the Kelly criterion, as he has referred to it on multiple occasions. He and his Berkshire Hathaway partner Charlie Munger both favor concentrated diversification, and the Kelly criterion is helpful in this.

Buffett stated: “I can’t be involved in 50 or 75 things. That’s a Noah’s Ark way of investing – you end up with a zoo that way. I like to put meaningful amounts of money in a few things.”

Examples of the Kelly Criterion

Kelly Criterion in Stock Markets

Trader Jack uses an approach with an average win rate of 40%, an average loss of $120, and an average win of $240. When he feeds these data points into the formula, he generates the following Kelly percentage:

Kelly Percentage = 40% - (1-40%) / ($240/$120) = 10%.

Therefore, Jack decides to use 10% of his account on each of his trades. He could also decide to take a more conservative approach, and use a fractional Kelly approach, using 5% of his account.

Kelly Criterion in Sports Betting

Gambler Jamie is at the Roulette table, and consistently bets on red, with odds of 48%. Because roulette has a one-to-one payout for betting on red, his average win is $20, while his average loss is the same, $20. Feeding this data into the formula, he generates the following Kelly percentage:

Kelly Percentage = 48% - (1-48%) / ($20/$20) = -4%.

As you may remember, a negative Kelly percentage should be interpreted as a recommendation to not follow this strategy – as it yields negative results over time. Jamie therefore decides to read up on more complex gambling strategies with better winning probability.

How Do Investors Use the Kelly Criterion Formula?

As discussed, traders on wall street and far beyond use the Kelly formula to calculate their optimal bet size. Warren Buffett used the formula to build his portfolio, to decide how much of the total Berkshire Hathaway funds he would use to buy his stake in companies like Chevron, Coca-Cola and Microsoft.

Application of Kelly Formula in Algo Trading

Because algorithms can clinically follow a systematic approach – the Kelly criterion is an excellent tool to calculate its optimal risk size. With ample data on its past performance, algo traders can optimize the strategy using Kelly’s formula, and take the profitability of algo-trading to the next level.

Read more about algorithmic and robotized trading here!

Kelly Criterion Limitations

Even though the Kelly criterion is a very useful model in portfolio management, it is not without shortcomings. Firstly, a mathematical model is only as reliable as the data it is feeded.

In this case, the Kelly criterion assumes you follow the exact trading system, with the same win rates as you did during the data it uses to calculate the optimal amount to bet. If these data points change, the Kelly calculation should be made again, to reflect these changes in the portfolio. This requires constant monitoring of trading or betting performance, which can be time-consuming.

Secondly, the Kelly criterion is aimed at seeking optimal returns, while some investors are more focused on long-term risk minimization, or cash flow from investments. This makes the Kelly criterion less suited for certain types of investors.

To sum up, the Kelly criterion is a mathematical approach to portfolio management, which can help calculate the optimal position sizing. This approach helps minimize drawdowns, while maximizing the long-term growth rate of your portfolio. However, it does not help with portfolio allocation or reduce volatility of the markets.

Nevertheless, it is important to keep track of your performance and expected returns, and make changes along the way. Exercise risk management, and do not blindly follow the Kelly criterion, but use common sense as well.

Writer’s Disclaimer: This article is based on my limited knowledge and experience. It has been written for educational purposes. It should not be construed as advice in any shape or form. Please do your own research.

This article contains links to third-party websites or other content for information purposes only (“Third-Party Sites”). The Third-Party Sites are not under the control of CoinMarketCap, and CoinMarketCap is not responsible for the content of any Third-Party Site, including without limitation any link contained in a Third-Party Site, or any changes or updates to a Third-Party Site. CoinMarketCap is providing these links to you only as a convenience, and the inclusion of any link does not imply endorsement, approval or recommendation by CoinMarketCap of the site or any association with its operators.

This article is intended to be used and must be used for informational purposes only. It is important to do your own research and analysis before making any material decisions related to any of the products or services described. This article is not intended as, and shall not be construed as, financial advice.

The views and opinions expressed in this article are the author’s [company’s] own and do not necessarily reflect those of CoinMarketCap.